The new changes in stamp duty that could save you thousands

On 3rd December 2014 Chancellor of the Exchequer George Osborne announced changes in ‘stamp duty’ that he said would benefit 98% of homebuyers. These changes would take effect from Thursday 4th December 2014. Saying that 98% of homebuyers would save money under new tax rules is an impressive soundbite, but what does it mean exactly?

What is stamp duty?

Stamp duty (its full title is Stamp Duty Land Tax and is often abbreviated to SDLT) is a tax that is applied by the government to the purchaser of a residential property, where the purchase price is more than £125,000. No stamp duty is applicable on a house purchase of less than £125,000.

Stamp duty must be paid within 30 days of completing on the purchase of a residential property.

What were the previous stamp duty rates?

Differing stamp duty tax rates were previously applied to the whole purchase price of the property.

| Purchase price | ‘Old’ SDLT rate |

| Up to £125,000 | Zero |

| Over £125,000 to £250,000 | 1% flat rate |

| Over £250,000 to £500,000 | 3% flat rate |

| Over £500,000 to £1 million | 4% flat rate |

| Over £1 million to £2 million | 5% flat rate |

| Over £2 million | 7% flat rate |

Previously, stamp duty was applied to the whole purchase price of the property, depending on which ‘band’ the purchase price fell into.

So for example, a residential house bought for £300,000 would have had the flat rate of 3% stamp duty applied to the full purchase price; so £300,000 x 3% = £9,000.

What are the new stamp duty rates?

While the stamp duty threshold remains the same (£125,000), there are now different banded rates.

| Purchase price | ‘New’ SDLT rate |

| Up to £125,000 | Zero |

| Over £125,000 to £250,000 | 2% |

| Over £250,000 to £925,000 | 5% |

| Over £925,000 to £1.5 million | 10% |

| Over £1.5 million | 12% |

Crucially, these rates are now applied differently.

Rather than the SDLT rate being applied as a flat rate on the whole purchase price, SDLT is now applied to the bands in a similar way that income tax is calculated.

So for example, a residential house bought for £300,000 would have the relevant SDLT rate applied in bands that only apply to the amount of purchase price that falls within each band.

- The zero rate is applied to the first £125,000 = £0

- The 2% rate is applied to the next £125,000 = £2,500

- The 5% rate is applied to the final £50,000 = £2,500

- Total stamp duty payable = £5,000

With the old ‘flat rate’ system, that £300,000 property would have generated stamp duty of £9,000.

This means that with the new banded system, the same property will now generate a stamp duty of £5,000; a saving of £4,000.

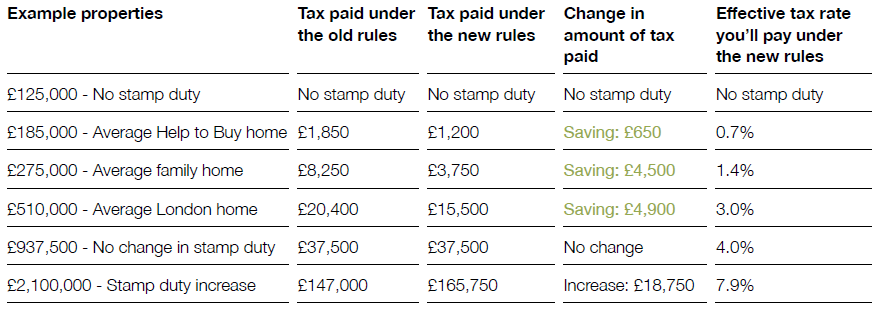

Stamp duty calculator

How would you benefit from these new legislative stamp duty changes? This table offers a quick guide to how you might benefit under the new SDLT rules.

The above figures have been taken from an excellent guide that has been published by HM Treasury, and is available here.

QualitySolicitors can help

Naturally, if you’re thinking about buying a house, then unexpected changes in legislation like this can be all too confusing along with everything else you’re trying to cope with.

That’s why getting a good solicitor can help give you peace of mind during what is often a very stressful experience.

At QualitySolicitors, we’re experts in all conveyancing matters. If you’re moving house, then call now on 08082747557 and talk to us for free to see exactly how we can ensure a smooth legal process for you from start to finish.